M&A and the Oil and Gas Endgame

Mergers & Acquisitions (M&A) can be an important tool for climate and transition and most companies are staking out their position in the endgame.

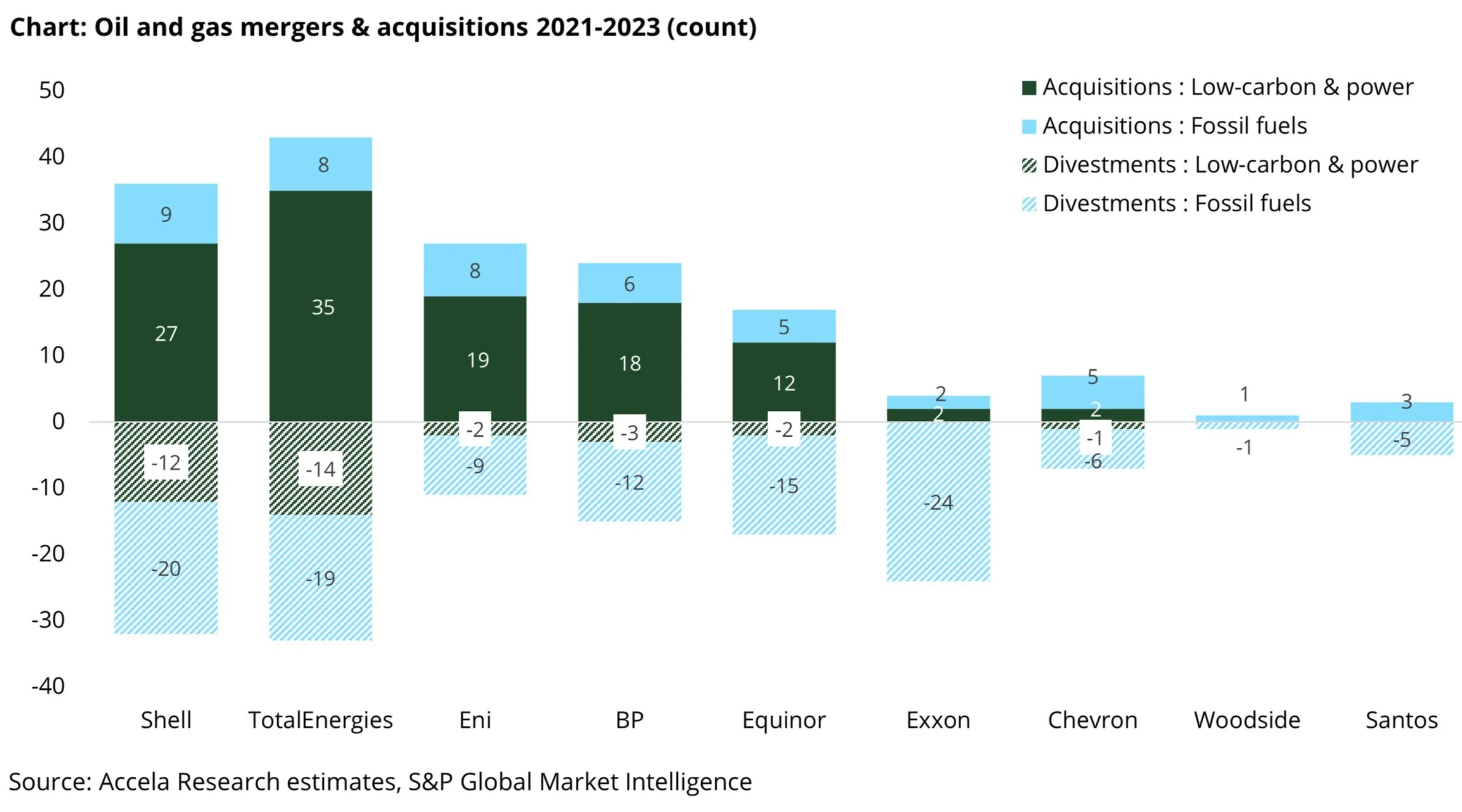

In this transition insight, we dive deeper into transactions of 9 oil and gas companies between 2021-23.

Our work finds the number of low-carbon & power acquisitions outpacing fossil fuels 2.5x, while fossil fuel divestments exceeded low-carbon 3.3x.

Key takeaways:

We see three strategic moves for forward-thinking oil and gas companies moving forward:

1) Exit the industry early before demand declines, minimising stranded assets and liabilities.

2) Diversification, following current customer demand trends to develop low-carbon energy, as a hedge to oil and gas revenue.

3) Efficiency, expand market share (consolidate), lower cost and carbon, focus on maximising cash and distributions.

-

TotalEnergies and Shell have made the highest number of low-carbon acquisitions and the highest number of fossil fuel divestments.

The largest low-carbon acquisitions were Archaea Energy (2022, $4.8bn renewable nature gas, RNG) and Shell’s acquisition of Nature Energy (2022, $2bn, RNG) both benefiting the potential sale of generated renewable fuel credits.

-

Announced acquisitions of Pioneer (Exxon) and Hess (Chevron) dwarf any recorded transaction size of other majors and are reflective of an attempt to increase scale and lower costs.

Exxon has had the most number of fossil fuel divestments, exceeding even European majors.

But together with Chevron lags behind European peers in the number of low carbon acquisitions (2 each).

Sizeable acquisitions by Exxon include CO2 capture firm Denbury ($4.9bn), and biofuel producer Renewable Energy Group (~$3bn)

-

M&A undertaken by Santos and Woodside are not reflective of a response to transition.

Both companies have no transactions in low carbon and power and little divestment of fossil fuels outside of project sell-downs.

Historic mergers with Oil Search (2021 Santos) and BHP Petroleum (2022 Woodside) provide these companies with access to larger balance sheets but don’t provide options in transition.